Woe to the taxpayer who runs afoul of the numerous and confusing IRA rules. There are forms to file, contributions to make, distributions to take, and penalties to avoid. While corrections are possible, it’s best to avoid mistakes in the first place. Here’s what you need to know.

IRAs come with a lot of rules, especially when it comes to taxes. Failure to follow the rules can result in penalties, excise taxes, double taxation, and in a worst-case scenario, the loss of your tax-deferred status. Here are a few tips that can help you avoid unnecessary—and costly—errors.

IRA CONTRIBUTIONS: ELIGIBILITY AND OPERATIONAL REQUIREMENTS

You must meet certain requirements to be eligible to make contributions to IRAs. Failure to meet these requirements can result in excess IRA contributions. Excess contributions that are not properly corrected can result in double taxation and excise tax being owed to the IRS. The following are some general eligibility requirements that must be met for IRA contributions.

Eligible income required. Regular IRA contributions must be made from eligible compensation, such as W-2 wages and/or salary, commissions, self-employment income, nontaxable combat pay, and other amounts earned from working.

• Special rule for spouses. If a wife, for example, does not earn income from working outside the home but is married to someone who does, her IRA contribution can be based on her working spouse’s income. In such cases, the couple must file a joint federal tax return.

• Contribution limit. The dollar limit for IRA contributions is the lesser of

(a) $6,000, plus $1,000 if you are age 50 or older by the end of the year, or

(b) 100% of the eligible compensation you receive for the year. As a result, if you earned only $3,000 for the year, the maximum amount that can be contributed to your IRA for the year is $3,000.

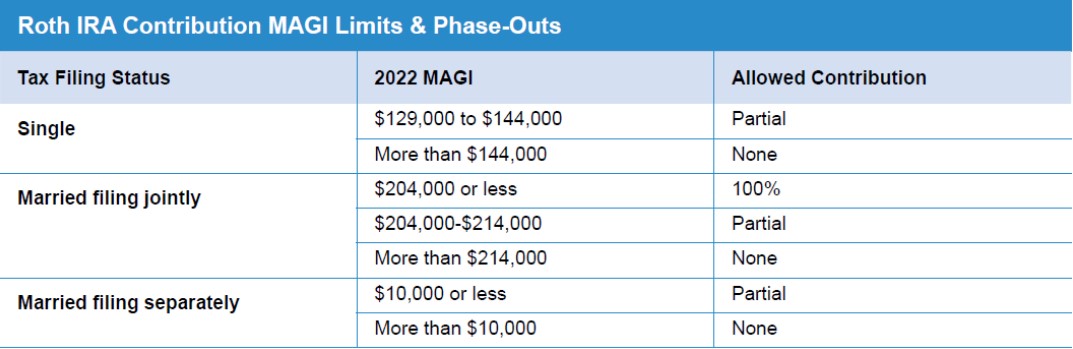

• MAGI limit. Contributions cannot be made to Roth IRAs if your modified adjusted gross income (MAGI) exceeds a certain amount. Roth IRA contribution limits are phased out if the MAGI falls within a certain range.

• Deposit deadline. IRA contributions must be made by your tax filing due date, which generally is April 15 for calendar-year tax filers. Tax filing extensions do not apply. If you make any contributions between Jan. 1 and April 15 for the previous year, you must clearly designate which year contributions apply. Failure to include that information may result in the IRA custodian applying the contribution to the current year.

Source: Appleby Retirement Consulting, Inc.

If you made IRA contributions and did not meet the income and age requirements where applicable, the contributions must be corrected under the “return of excess contributions” procedures.

Under these procedures, excess contributions must be removed by your tax filing due date plus extensions and must be accompanied by any net income attributable (NIA) to the contributions. NIA can be earnings or losses and are determined using an IRS-provided formula. If the IRA custodian will not perform the calculation, the formula—which can be found in IRS Publication 590, Individual Retirement Arrangements (IRAs)—can be used.

BASIS-RELATED ACTIVITY

IRS Form 8606, “Nondeductible IRAs,” must be filed to report basis-related activity, including nondeductible contributions made to traditional IRAs, and distributions/Roth conversions from traditional IRAs if you have any basis in any traditional IRA.

REPORTING NONDEDUCTIBLE CONTRIBUTIONS

Nondeductible traditional IRA contributions and rollover of after-tax amounts from an employer-sponsored retirement plan—such as a 401(k) plan—creates basis in the IRA. IRS Form 8606 must be filed for every nondeductible contribution made to traditional IRAs. Failure to file Form 8606 to report a nondeductible IRA contribution may result in a penalty of $50 being owed to the IRS unless you can show “reasonable cause” for the failure.

AVOIDING DOUBLE TAXATION FOR DISTRIBUTIONS OF BASIS

Generally, distributions from IRAs are treated as taxable income. However, distributions of basis amounts are not taxable. Unfortunately, many individuals pay income tax on basis amounts because IRS Form 8606 was not filed when it should have been.

To prevent this from occurring, IRS Form 8606 must be filed for any year you make a withdrawal or convert amounts from a traditional IRA, if the IRA has basis. For this purpose, all your traditional IRAs, SEP IRAs, and SIMPLE IRAs are treated as one traditional IRA.

Form 8606 and its instructions helps you, the IRS, and other interested parties determine the non-taxable portion of IRA distributions and conversions.

CLAIM EXCEPTIONS AND PAY PENALTIES

IRS Form 5329, “Additional Taxes on Qualified Plans (Including IRAs) and Other Tax-Favored Accounts,” is used to report additional taxes such as the:

• 10% early distribution penalty on distributions that occur before the account owner reaches age 59½

• 6% excise tax on excess contributions that are not corrected by the applicable deadline

• 50% excess accumulation penalty on required minimum distributions (RMDs) that are not withdrawn by the deadline

THE 10% PENALTY

Distributions that are made from retirement accounts before you reach age 59½ are subject to a 10% early distribution penalty unless an exception applies. In some cases, IRA custodians will indicate that an exception applies by inputting the applicable code

in Box 7 of IRS 1099-R, “Distributions from Pension, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc.”

Form 1099-R is used to report distributions from retirement accounts. If you qualify for an exception, but the custodian does not input the exception code in Box 7, Form 5329 can be filed to claim the exception. Form 5329 can also be filed if the custodian incorrectly indicates that an exception applies, when it does not.

THE 6% EXCISE TAX

Generally, excess contributions and ineligible rollover amounts that are not corrected by the tax filing due date—including extensions—are subject to a 6% excise tax for every year the amount remains in the IRA. In such cases, the penalty must be calculated and reported on IRS Form 5329.

THE 50% ACCUMULATION TAX

You must begin taking RMDs from your traditional, SEP, and SIMPLE IRAs for the year you reach age 72 and continue for every year thereafter for as long as you live.

Generally, RMD amounts must be withdrawn

by Dec. 31 of the year for which they are due. An exception applies for the year you reach age 72, allowing the RMD for that year to be taken as late as April 1 of the following year.

If you miss an RMD deadline, you will owe the IRS

a 50% excess accumulation penalty on the RMD shortfall. The IRS will waive the penalty if the deadline was missed due to “reasonable cause.”

IRA owners who miss their RMD deadlines must file IRS Form 5329 to either report and pay the penalty, or request the waiver if eligible.

PREVENTION IS BETTER THAN CURE

While operational failures and ineligible contributions can be corrected, it is usually more practical and less costly to prevent them from happening in the first place. Talk to your financial professional and/or a tax professional for guidance on how to prevent costly mistakes.

Risk Disclosure: Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results.

This material is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. The content is developed from sources believed to be providing accurate information; no warranty, expressed or implied, is made regarding accuracy, adequacy, completeness, legality, reliability or usefulness of any information. Consult your financial professional before making any investment decision. For illustrative use only.

Fee based financial planning and advisory services offered by Genesis Wealth Management Group, LLC, an Independent Registered Investment Advisor.

Copyright © 2022 by Horsesmouth, LLC. All rights reserved.

This reprint is provided exclusively for use by the licensee, including for client education, and is subject to applicable copyright laws. Unauthorized use, reproduction or distribution of this material is a violation of federal law and punishable by civil and criminal penalty. This material is furnished “as is” without warranty of any kind. Its accuracy and completeness is not guaranteed and all warranties expressed or implied are hereby excluded.